Does going to college make financial sense anymore?

Past generations saw college as a guarantee of a higher salary and a leg up in the job market, but many families today wonder whether it’s still worth it. Recent shows tuition prices have risen significantly, averaging more than $45,000 per year at private, nonprofit four-year institutions. Public four-year colleges are offering out-of-state tuition for just shy of $32,000 per year. High tuition costs, plus the tougher job market, mean that a degree doesn’t necessarily guarantee good career prospects.

Regarding whether college is still worth it, the short answer is yes, but with some important conditions. The data still supports a financial return on a college education, but it’s important to make sure that the cost of college and the amount of debt you take on make sense for your major and career path.

If you or your child is considering college, this guide from can help you understand what the data shows, the real ROI on college, and whether it’s worth considering alternatives.

The short answer: College can still pay off, but not in every case

When you’re weighing whether to attend college, the right question isn’t “Is college worth it?” Instead, the right question to ask is “Will this degree, at this price, for this career path, produce a reasonable return?” By asking that question, you’ll get a more accurate view of whether college is worth it in your very specific situation.

confirms that weekly earnings for someone with a bachelor’s degree are still considerably higher than for someone with no degree. However, that data doesn’t take into account every single career path, nor does it show the ROI based on how much you spend on your education.

So, as you’re deciding whether college is right for you, don’t just look at the average numbers. Look at your specific situation, how much you’ll pay for school, and how much you’ll likely earn after graduation, and use that to decide if the payoff is there.

Why people are questioning the value of college more than before

College enrollment peaked in 2010 and has decreased since then. Roughly attended graduate or undergraduate programs in 2010. By 2024, that number was just over 19 million. There are a few key reasons for this change:

- Rising tuition and living costs: The cost of higher education has , with a compound annual growth rate of 4.04%. Compare that to the overall inflation rate, which was , and you can see that college costs have risen disproportionately. When you add that to the overall higher cost of living today, many people no longer see it as feasible to attend college.

- Greater sensitivity to debt: The average student loan debt is as of 2025. With a total student loan debt of , the tolerance for taking on debt for school isn’t what it once was. Borrowers today are more aware of what their level of debt means — perhaps because the parents of today’s college-aged students are, in many cases, still paying off their student loan debt.

- More visibility to alternatives: While college was once seen as the best option, people have become more aware of the alternatives available, including apprenticeships, trade programs, associate degrees, certifications, and boot camps. Some of these offer a far faster path to the workforce with less (or no) debt.

- Outcome-based decision-making: Millions of families are now doing exactly what you are — they’re running the numbers to determine whether college actually makes sense from an ROI perspective. If they aren’t happy with the numbers they see, they may opt for alternatives.

What the data still says about earnings and employment

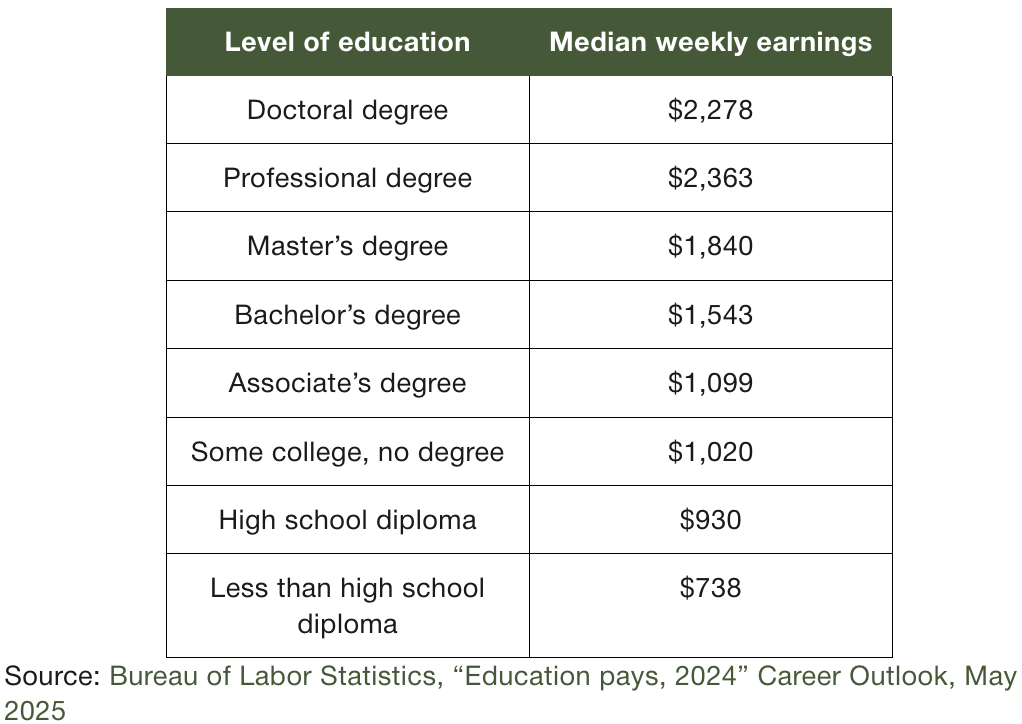

Degree holders still tend to earn more

Data from the BLS shows that workers with bachelor’s degrees earn upward of $600 more per week than those with only a high school diploma and about $500 more than those with some college but no degree. These differences add up to tens of thousands of dollars over the course of a year.

The table below breaks down the median weekly earnings for people at various levels of education, according to 2024 data.

While these numbers don’t guarantee any personal outcomes, they do show us that, for the most part, people with college degrees are earning more than people without them, and the difference is still relatively significant.

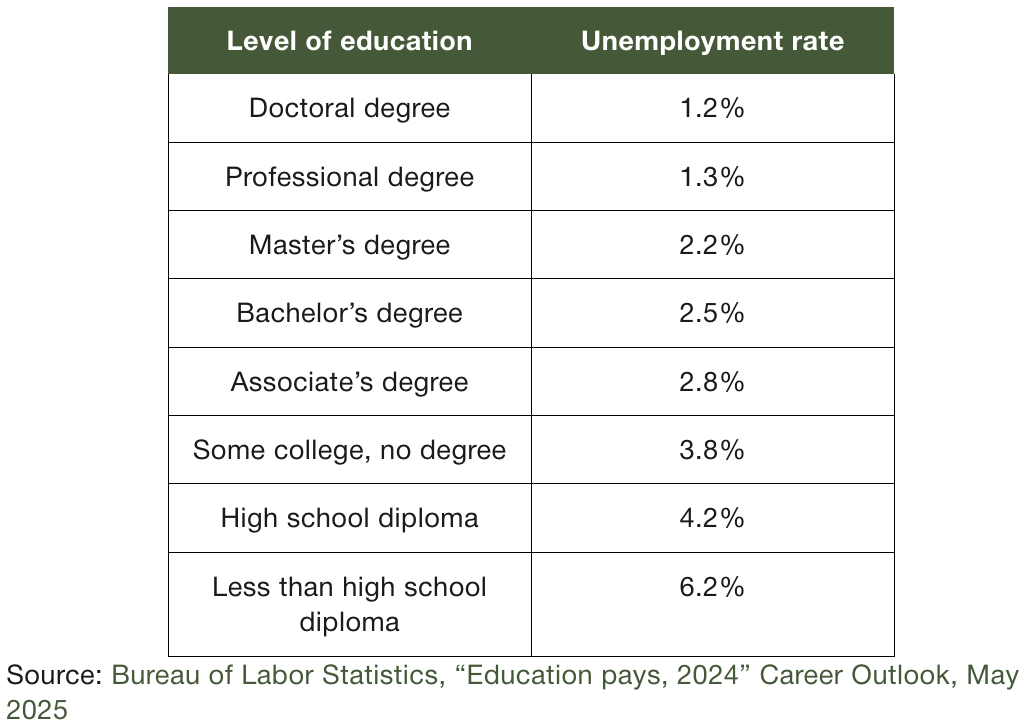

Unemployment risk tends to be lower with more education

In addition to wages being higher for workers with college degrees, they also face lower unemployment rates. Those with doctoral and professional degrees face the lowest unemployment rates of all, while those with no high school diplomas or only high school diplomas face considerably higher unemployment rates.

In reality, this means that with a college degree, you’re less likely to have periods where you aren’t earning income. In the long run, this increases your lifetime earnings and leads to fewer circumstances of severe economic stress.

The table below breaks down how unemployment rates vary across different levels of education:

The catch: College ROI varies a lot by school, major, and debt load

At first glance, the numbers show us that college can be worth the price tag. But it’s not quite that simple, as the actual ROI varies depending on your college, tuition price, amount of debt incurred, and career choice.

Not all colleges deliver the same financial return

The cost of college doesn’t look the same everywhere. The cost of attendance ranges from an average of . Generally speaking, private and out-of-state schools carry higher price tags, while public in-state schools are the cheapest.

Total cost isn’t the only factor that matters. Georgetown University’s Center on Education and the Workforce . It looks at the actual median earnings from students who attended that school compared to the net price at the institution. Colleges with higher price tags could have higher ROIs if their graduates often go on to earn higher salaries.

In fact, by taking a look through the database, you’ll see that many top-ranking schools also have higher price tags. MIT, Stanford, and Princeton all appear on the first few pages, not because they’re the cheapest, but because they have an excellent ROI, according to the study’s findings.

Major choice can shape the payoff

You probably won’t be surprised to find that your college major and ultimate career path will have a major impact on your college ROI. The reports that the bachelor’s degrees with the highest lifetime ROI include:

- Finance

- Computer and information sciences

- Computer engineering

- Economics

- Electrical engineering

- Accounting

- Management systems and statistics

- Chemical engineering

- Mathematics

- International relations

That doesn’t mean you can only earn a high salary if you major in one of these fields, nor does it mean everyone who majors in one of these fields will earn a lot of money. However, majoring in one of these does give you the highest chances of a high ROI on your college degree.

Net price matters more than sticker price

The sticker price of a college isn’t necessarily what you’ll pay. Instead, your total cost is the net price, which is what’s left after financial aid.

Certain types of financial aid are need-based, meaning they go to the students with the greatest financial need, usually with household incomes under a certain level. Meanwhile, merit-based aid usually goes to the students with academic or athletic achievement.

Some have large aid packages to help make their high tuition prices more affordable, especially for low-income families. While their sticker prices may be higher, you could actually end up paying less out of pocket.

When college usually makes financial sense

The answer to when college makes financial sense isn’t the same for every student or family. Generally speaking, college might be a good financial decision if some or all of the following are true:

- The student has a clear career path that commonly requires a degree.

- The family can keep borrowing under control.

- The student is likely to graduate on time.

- The school has solid completion and outcome data.

- Aid or savings meaningfully reduce net cost.

Careers where a degree is often the entry ticket

There are some careers where a degree is necessary to obtain employment. For example, you likely can’t get a job as a registered nurse, K-12 teacher, or engineer without a degree. Additionally, many corporate roles require degrees, even if they aren’t as specialized.

This factor is one of the most important to consider when weighing your education options. If you’re set on a career that requires a degree, that may help answer your question.

The role of planning before enrollment

Don’t wait until it’s time to enroll in college to start planning the financial side of it. There are plenty of , and you can make the most of them with careful planning, which includes comparing costs and aid packages, understanding your expected salary, and researching your savings options, all while minimizing debt.

When college may not make financial sense

Just like there are some situations where college clearly makes sense, there are others where it might not make as much financial sense. Some examples of those include:

- A student has no clear major or career direction.

- There’s a high projected debt compared to the expected earnings.

- There’s a low likelihood of finishing on time (or at all).

- The student might benefit from working first, then returning later with better clarity.

- The career path doesn’t require a degree for maximum earning potential.

Alternatives that may offer stronger short-term ROI

College isn’t right for everyone, and some alternatives still offer great ROIs. These options may be especially beneficial for someone who doesn’t need a four-year degree to make good money in their chosen career, or students who don’t thrive in school. Options include:

- Trade school

- Apprenticeships

- Certificate programs

- Associate degrees

- Employer-sponsored education pathways

A key benefit of these alternatives is that you can still . If you’ve been saving for your child’s college education and they aren’t sure it’s right for them, this factor can give you plenty of peace of mind that your savings can still be used effectively.

How families can lower the real cost of college

If you’re getting ready to send a child off to college, there are some steps you can take to lower your out-of-pocket costs and increase your child’s ROI.

Start with aid before loans

The Federal Application for Federal Student Aid (FAFSA) puts your child in the running for federal financial aid. Depending on your household income, it could make your child eligible for , work-study programs, and federal loans. Additionally, your child may apply for private scholarships to help lower their costs.

When planning your financing, make sure to prioritize free aid like grants, scholarships, and work-study programs before turning to student loans, since you don’t have to pay them back.

Use 529 plans strategically

A 529 plan helps you save for college in a tax-advantaged way. As long as you use the funds for qualified expenses, you won’t pay taxes on your investment earnings. Additionally, you can use some of the money to repay student loans. And thanks to more recent legislative changes, some unused funds can get rolled over into a Roth IRA later on.

When saving for college, there’s a clear benefit to starting early, as your money has time to grow and compound. However, starting late is better than starting never. Any money you can set aside in a 529 plan will get your child one step closer.

Compare schools based on net price, not brand alone

It’s tempting to choose a school based on the one with the most prestigious name, but they don’t always correlate with the highest salary later.

Use tools like to compare the average annual cost, graduation rates, typical debt, and median earnings for any school you’re comparing. Additionally, Georgetown’s ROI rankings can give you an idea of which schools offer the most bang for your buck.

Finally, use the to get an idea of how much aid your child might get based on your household income. This can help you set your family’s savings goals to reduce the amount of debt your child has to take on.

What to check before saying yes to any school

Before committing to enrollment or signing for any student loans, run through these questions to make sure a school and career path are right for you.

- What will the degree actually cost after aid? Make sure to look at the net price rather than the published tuition price, as it represents your actual out-of-pocket costs.

- How much would you need to borrow? Consider the common rule of thumb that advises against borrowing more than you will earn in your first year after college.

- What do graduates from that school or program tend to earn? There’s clear data showing earnings information broken down by school. You can see the ROI after 10, 20, 30 years, and on.

- What is the graduation rate? Schools with lower graduation rates are a red flag, especially if they also have higher price tags or borrowing.

- Could a lower-cost path get you to the same goal? Is there a more affordable school or alternative program type that could get you to the same employment outcome?

- What happens if the student changes direction? Many students change majors at least once. Consider how your costs or timeline might change if that happens.

- How will this choice affect the family’s broader financial plan? Your child’s college education is just one part of your family’s financial plan. It’s important to take a holistic look at your family finances and how college funding fits in.

If student loans are part of the plan, borrow carefully

If you’re taking on debt to pay for college, the calculation, unfortunately, may look a bit different. In addition to the actual cost of college, you’ll also have to factor in your total interest costs, which can considerably increase your total price tag.

One common rule of thumb that experts recommend is that your total debt amount shouldn’t exceed your first-year salary after graduating.

Additionally, it’s not just about the amount of debt you’re taking on. It’s also about the type of debt. Federal loans carry more protections for borrowers, including income-driven repayment options, deferment and forbearance provisions, and loan forgiveness pathways. Private loans don’t offer those same protections.

For families already managing student loan debt, that can help you determine the best way to pay off your debt for the lowest cost.

The bottom line

College is more expensive than ever, but it can still be one of the best investments a person can make in their career, especially in the right career path. Rather than operating under a base assumption about whether college is worth it, run the numbers for your unique situation as it relates to your college major, the net price at your desired school, and your potential earnings after graduation.

The best college choice isn’t necessarily the most prestigious or expensive one; it’s the one where the numbers make sense for you and your goals.

FAQs

Is college still worth it financially in 2026?

The data shows that college is still worth it in 2026. Workers with bachelor’s degrees earn significantly more and face lower unemployment rates than workers without degrees. However, you’ll have to run the numbers for your specific situation to determine if it’s really worth it for you.

What makes a college degree worth the cost?

The most important factors that drive college ROI are the net price (your cost after aid), graduation odds, and career payoff. A low price tag paired with a high chance of graduation and high post-grad earnings is a great sign for a positive ROI.

Is trade school better than college financially?

Trade school doesn’t necessarily have a higher payoff than college, but it can in some situations. It’s often more affordable and doesn’t take as long to graduate. As a result, you’re earning money faster than if you went for a four-year degree. If your career path is one that would benefit from trade school rather than a bachelor’s degree, it’s definitely worth considering.

How can I estimate whether a school is worth it?

There are plenty of online resources like College Scorecard and Georgetown’s college ROI rankings that can give you an idea of whether a particular school is worth it based on its price tag, graduation rates, and how much you’re likely to earn after graduation. Make sure to pay special attention to the prospects for your specific program.

Can a 529 plan still help if my child does not attend a traditional four-year college?

Yes, 529 plans can be used for many different education costs, including trade schools, apprenticeships, and even student loans. If your child , you can also change the beneficiary to someone else or roll the money into a Roth IRA for your child.

Prior to investing in a 529 Plan, investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

was produced by and reviewed and distributed by şÚÁĎÉç.